While announced last year, the acquisition of Mexican chocolate manufacturer Grupo Turin by international behemoth Mars has only recently been completed.

The move makes sense for a number of reasons - Mexico is a fast-growing market for chocolate, achieving an 11% value sales CAGR between 2010 and 2015 to become a billion-dollar market; more cynically, the move disrupts a preexisting distribution arrangement premium player Lindt had with the Mexican company.

Indeed, Mars may find itself treading on Lindt's toes further due to Grupo Turin's extensive portfolio of premium chocolates, and moving into this segment of the market is long overdue for the company.

Mars likely to experiment with Grupo Turin brands internationally

Grupo Turin is a relatively modestly sized company, with a 3% share of the Mexican market, or $33m in sales - this is just 14% of Mars' sales in Mexico.

However, given Turin specializes in premium chocolate - an area Mars has been notably absent in - it appears that Mars is using the acquisition as a controlled test for expanding its premium portfolio.

Unlike a handful of its rivals, Mars' company culture generally promotes patience and long-term planning over short-term gains.

This generally explains the company's success in moving into new international markets where others have been conspicuous in their failure. With the acquisition, it seems probable that Mars will begin testing out Turin's premium brands in the US.

Mars' predilection for patience is usually its strong suit, but there may be flaws at this point.

Late to the party ?

Premiumization has been a buzzword in chocolate for at least half a decade, and Mars is the last of the "big six" - along with Lindt, Ferrero, Nestlé, Hershey and Mondelēz - to invest in the market.

Nestlé has recently announced plans to distribute premium chocolates Cailler and Baci Perugina internationally, accompanied by extensive marketing campaigns; Mondelēz possesses several premium brands; Hershey has also made moves in the market; while Ferrero and Lindt naturally have a strong position owing to years of operating in the premium space.

Taking into account its acquisition of Russell Stover, Lindt's market share has increased by over two percentage points in the last five years; Mars' share has decreased by one percentage point.

Too little, too late?

The reasons for this shift boil down to improved profitability within premium chocolate as well as the sclerotic volume growth in key Western markets, particularly the US; the mass chocolate market has steadily become more saturated, hence a race to the top where there is greater room for innovation, sales growth and share gain.

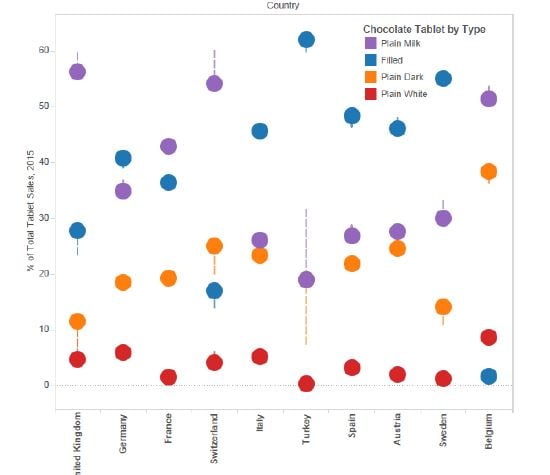

As the graph below shows, there has been a movement towards filled and dark tablets between 2007 and 2015 - there generally tends to be greater scope for premium ranges for these types of tablets, with companies adding new ingredients such as salted caramel, chilli and sea salt in particular over this time period.

Tablet Sales by Type in Western Europe, 2007-2015 (%)

[Note: Dashed lines indicate growth from 2007]

Mars is arguably acting more slowly and less substantially than its competitors, risking an unfashionable, rather than fashionably late, arrival at the party.

By the time its products become widely available, consumers may have developed greater loyalty to, for example, Lindt, or Nestlé's Damask or Cailler brands.

The danger for all of these manufacturers is that the saturation that has occurred in mass-priced chocolate will simply be recreated in the exalted heights of premium chocolate.

There is a limit to how 'premium' mass manufacturers can go before prices become unattractive to consumers.