Cocoa requires consistent rainfall with periods of intermittent sun exposure to thrive. The high volume and intensity of the rainfall has led to widespread droppage of the flowers that turn into cocoa pods after 22 weeks.

Further, it has accelerated the spread of a fungal disease called black pod which rots developed cocoa pods and destroyed one-tenth of Ghana’s last cocoa harvest. To compound the weather impacts, high inflation in the region has created a cash crisis in which cocoa suppliers are unable to access affordable fertilizers and pesticides and cannot pay for labourers and farmers.

With the crop damages inflicted by the rains and the outbreak of disease, and the potential labour shortages due to non-payment, the global supply of cocoa is at considerable risk. Manufacturers of chocolate and confectionery products, reliant on cocoa inputs, have already begun raising consumer pricing due to the sourcing challenges.

Poor growing conditions in West Africa threaten cocoa production

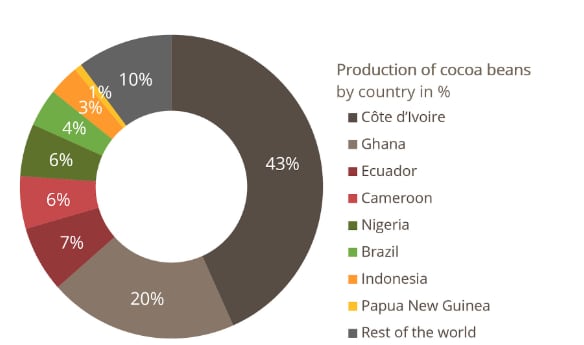

From March to October, West Africa experiences its primary cocoa growing season, followed by the harvest season from November to February. The recent growing season in Cote d’Ivoire, the largest producing country, was the wettest so far this century. The impressive rainfall amounts surpassed the levels observed in the second and third wettest seasons of the past two decades, which occurred in 2014 and 2010. Notably, this season witnessed early and sustained anomalous wetness, posing an increased risk of mould and diseases throughout, thereby affecting both the quality and quantity of cocoa production.

Supply disruptions prompt cocoa price increases for end-users, enabling new competition

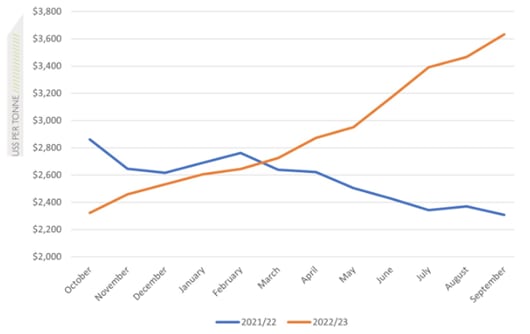

Amid the production disruptions in the world’s top cocoa-producing region, a third-consecutive global cocoa deficit is expected. In the 2022-23 season, there was a recorded deficit of 146,000 metric tons, which is expected to be surpassed this season given the worsening conditions. Amid these concerns, cocoa trading prices have surged to 46-year highs.

Due to general inflation trends, consumers in Europe and the US have already seen price increases of 13% and 20%, respectively, for chocolate products over the last two years. While demand for chocolate has held strong in top chocolate-consuming countries amid the constant price increases of recent years, additional pressure from global sugar shortages has affected the industry this year. Manufacturers like Hershey and Mondelez have already reported price increases at the consumer level for some of their products to off-set the inflated costs of production.

For both companies, price increases have been met with declines in chocolate sales volumes and growth forecasts. Even in Switzerland, the top country for chocolate consumption per capita, consumer purchasing has declined. Swiss-Belgian cocoa processor and chocolate manufacturer Barry Callebaut AG reported in May, before the summer weather impacts occurred, that sales volumes fell nearly 3% year-to-date. The new wave of challenges to cocoa production is expected to prompt unprecedented price hikes and, with them, an uptick in private label competition for consumer spending.

As chocolate and confectionery products are largely treated as a treat, rather than a necessity like other food products, private label competition has historically been low. For general consumer goods in Europe, private label brands are 37.8% of total value sales, with the highest penetration in markets in Spain at 47%, Germany at 41%, and the Netherlands at 40%.

This has typically excluded chocolate products as consumers are more willing to pay a premium price for the branded item for specialty products. In 2022, private label chocolate products made up only 2.7% of the US retail market, whereas private label dairy products, for example, make up 62% of sales. However, the unprecedented cocoa price hikes experienced this year have paved the way for lower-cost, private chocolate labels to penetrate the market and attract new consumer interest. In the US, private label sales for chocolate grew 9% year-to-date by June. Many expect this trend to stick, with global forecasts of a 5.45% compound annual growth rate (CAGR) for private labels between 2023-2030.

Outlook and recommendations

Due to the production challenges, bean deliveries to ports in Cote d'Ivoire are behind 16% already this season. Exporters cite needing 150,000 tons of cocoa beans to avoid defaulting on their contracts. Cocoa regulators in the country have already scrapped a stockpile exemption for bean grinders which gives them an advantage over traders and permits stockpiling beans beyond their contract allowance. This year, that exemption would likely put cocoa suppliers in a position where they would be unable to meet their commitments.

However, it is also likely to trigger impacts on end-users quicker, as chocolate products depend on grinding as an integral part of the processing for end-use consumption. If other producing countries like Ghana or Nigeria implement similar protocols, the effects on the chocolate and confectionery industries will be amplified. Though this would impact both brand name and private labels, the latter operates with smaller batches and would be less vulnerable to supply decreases. Further, El Nino threatens to bring extreme dryness to West Africa, which could impact the next cocoa harvest and prolong the supply shortages.

- Jon Davis is chief meteorologist at Everstream Analytics.